Evidence Debt: Why Finance Teams Can Post a Transaction but Can’t Prove It Fast

Evidence Debt is the backlog of transactions your finance team can record, but cannot explain quickly when close, audit, refund review, or e-Invoice support pressure arrives.

Month-end does not usually break because the numbers are completely wrong.

It breaks because the proof is scattered.

A sale sits in the POS export. The settlement sits with the payment provider. The receipt sits at the outlet. The refund approval sits in a WhatsApp message, email thread, or manager note. The consolidated e-Invoice record sits somewhere else.

Each piece exists.

But when finance needs to explain the transaction, the chain is weak.

That is Evidence Debt.

Evidence Debt is the backlog of transactions your team can record today, but cannot prove quickly when close, audit, refund review, or compliance support pressure arrives.

For a multi-outlet F&B finance team in Malaysia, this is not a paperwork problem. It is a finance workflow problem.

It slows close. It weakens audit-readiness. It turns refund review into detective work. And it forces finance to depend on outlet follow-ups when the evidence should already be ready.

The real problem is not “missing receipts”

Most teams describe the issue as receipt-chasing.

That is only part of it.

The deeper issue is that the evidence chain is incomplete.

A transaction is not truly proof-ready just because one document exists. It is proof-ready when finance can connect the key pieces without guessing:

- the outlet where the transaction happened

- the receipt or sales record that shows what happened

- the payment rail that moved the money

- the settlement or payout record that shows what cleared

- the refund or adjustment record, if one exists

- the GL entry or close file where the transaction ended up

- the e-Invoice support needed for the period

If those pieces cannot be linked quickly, finance carries Evidence Debt.

The transaction may be posted.

But it is not audit-ready by default.

What Evidence Debt looks like during close

Picture Day 4 of close.

Your team is trying to finish the sales and payment review for several outlets. The numbers look close enough to keep moving, but a few items need support.

One outlet has a refund that appears in the payment report but is not clearly tied to the original receipt.

Another outlet has a delivery-platform settlement that does not match neatly to the POS export.

A card payment appears in the bank settlement file, but the reference does not point cleanly back to the outlet sale.

A manager says the receipt was printed and kept at the outlet, but no one can find the image or attach it to the close folder.

Nothing looks criminal.

Nothing necessarily means the accounts are wrong.

But the finance team cannot answer the simple question fast enough:

Can we prove this transaction from outlet to payment to settlement to books?

That is where the time goes.

Not in accounting theory.

In chasing evidence.

The cost is practical

Evidence Debt shows up as small delays first.

Then it becomes a pattern.

Finance waits for outlet managers. Outlet managers search old folders, WhatsApp threads, POS screens, or printed receipt stacks. Someone downloads another payment report. Someone checks whether the refund was approved. Someone asks whether the settlement was net of fees. Someone tries to match the number manually.

By itself, each case feels small.

Across multiple outlets, payment rails, and close periods, the pattern becomes expensive.

Evidence Debt creates:

- slower close support

- weak audit defensibility

- refund traceability gaps

- unclear outlet-level proof

- settlement matching issues

- duplicated follow-up work

- more pressure on finance during review periods

- higher dependence on memory and manual chasing

A clean way to say it:

You can record the transaction. You just cannot prove it fast.

That is the problem you feel when your team is responsible for close support, audit evidence, refund review, and transaction records across multiple outlets.

Evidence Debt usually has three failure modes

Evidence Debt tends to come from three breaks in the chain.

1. Outlet proof exists, but it is not finance-ready

The outlet may have a receipt, POS record, refund note, or manager approval.

But finance cannot easily retrieve it, trust it, or connect it to the close file.

What it looks like:

- receipts stored differently by outlet

- screenshots instead of structured records

- refund approvals kept outside the finance workflow

- missing outlet identifiers

- inconsistent naming rules

- unclear links between receipt, refund, and sales record

What it breaks:

Finance has to reconstruct what happened instead of reviewing evidence that is already organized.

2. Payment proof exists, but it does not connect cleanly

The payment report, bank line, wallet report, or PSP record exists.

But the reference does not tie cleanly back to the outlet sale, receipt, or refund.

What it looks like:

- settlement files grouped by batch instead of transaction

- different references across POS, payment provider, and bank

- fees or deductions changing the final amount

- payment reports that do not preserve useful outlet-level context

- delivery-platform or wallet payments that need manual matching

What it breaks:

Finance can see money moved, but cannot always explain the full path without manual work.

3. Close proof exists, but the chain is not defensible

The transaction is posted. The close file may even be complete enough to move forward.

But if someone asks for support, the evidence is not easy to pull, explain, or defend.

What it looks like:

- GL entries with weak supporting references

- close folders that depend on attachments without context

- refund adjustments that require a story to explain

- consolidated e-Invoice support that is disconnected from outlet-level records

- audit samples that trigger a last-minute evidence hunt

What it breaks:

Finance spends time proving what should already be connected.

The better question is not, “Do we have the receipt?”

That question is too narrow.

A receipt is only one evidence object.

The better question is:

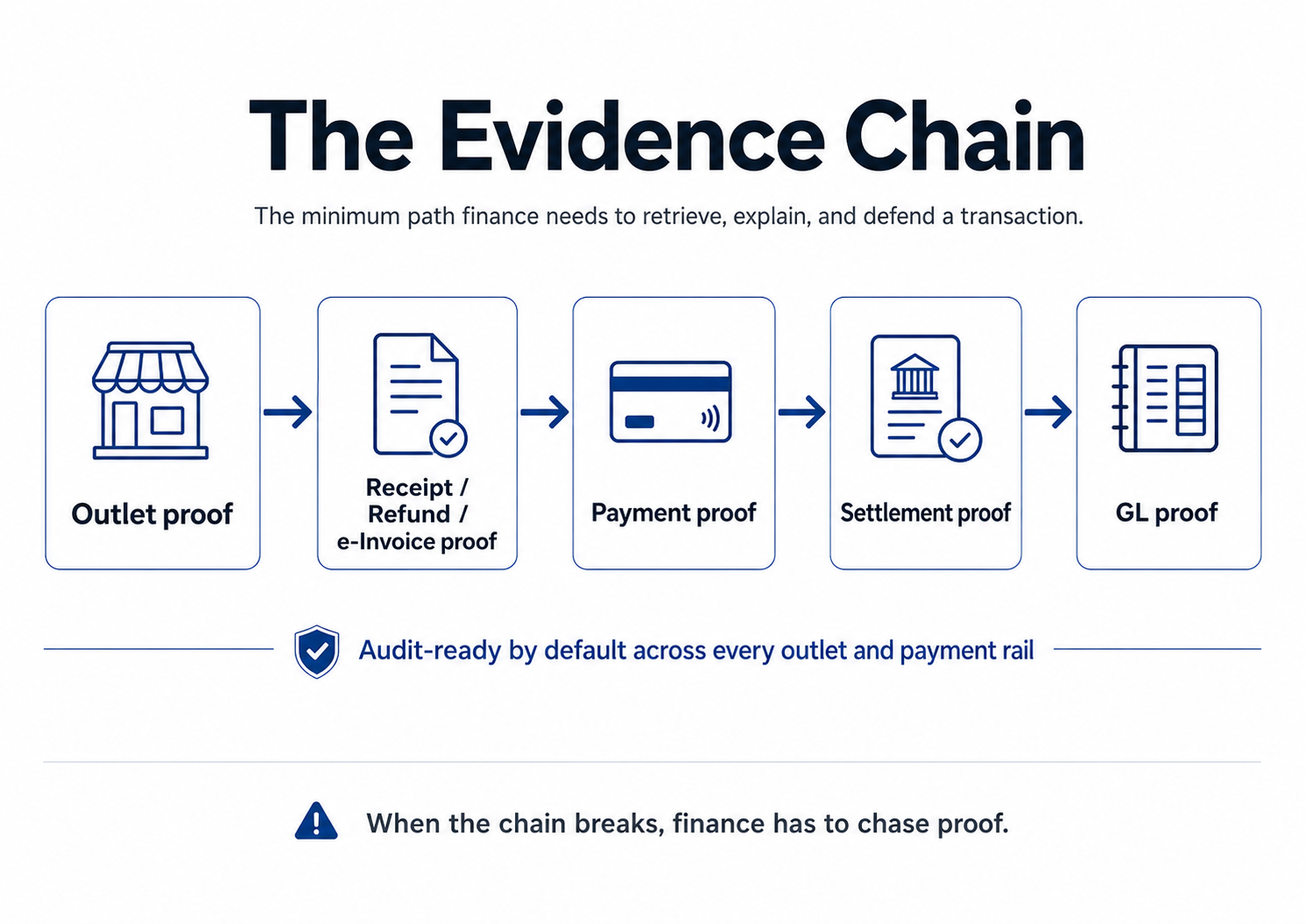

Do we have an evidence chain?

For a multi-outlet F&B finance team, an evidence chain should connect:

Outlet proof → payment proof → settlement proof → GL proof

That does not mean every process needs to be perfect.

It means the minimum proof should be retrievable, organized, and defensible when finance needs it.

At minimum, the team should be able to answer:

- Which outlet did this transaction come from?

- What receipt, sales record, refund record, or e-Invoice support explains it?

- Which payment rail moved the money?

- What settlement or payout record confirms what cleared?

- Where did it land in the books?

- Can finance retrieve the support without chasing three people?

If the answer is no, the team has a Proof Gap.

The two-minute test

Here is a simple way to test Evidence Debt.

Pick 10 transactions from the last close period. Include a mix of normal sales, refunds, wallet payments, card payments, delivery-platform settlements, and any items that usually create questions.

For each transaction, ask:

Can finance pull the evidence chain in under two minutes without guessing?

Not eventually.

Not after asking the outlet.

Not after searching five folders.

In under two minutes.

A transaction passes if finance can quickly connect the outlet record, payment record, settlement record, and close support.

A transaction fails if the team has to chase, reconstruct, rename, explain from memory, or depend on one person who “knows where it is.”

That failed item is Evidence Debt.

A practical one-week fix plan

You do not need to boil the ocean.

Start where Evidence Debt is created most often.

Day 1: Sample the pain

Pull 25 transactions from the last close period.

Choose the items that usually create friction:

- refunds

- delivery-platform settlements

- wallet or QR payments

- card settlement exceptions

- outlet-level adjustments

- transactions with weak references

- items that required manager follow-up

Do not start with the biggest transactions only.

Start with the transactions that waste the most finance time.

Day 2: Classify the break

For each item, classify the main break:

- outlet proof problem

- payment proof problem

- settlement proof problem

- GL or close support problem

- refund traceability problem

- e-Invoice support problem

The goal is not perfection.

The goal is to see where the chain breaks most often.

Days 3–4: Standardize one join point

Pick one evidence link and make it consistent.

Examples:

- require one outlet identifier in the close support

- require one payment reference on refund records

- require one settlement batch reference for wallet or PSP reports

- require one naming rule for receipt images or exported files

- require one close-folder structure for each outlet

Do not redesign the whole finance system.

Fix one link that reduces chasing.

Days 5–7: Reduce the top two drivers

Look at the sample again.

Which two proof gaps created the most delay?

Fix those first.

If refund proof is the biggest issue, standardize refund evidence.

If settlement matching is the biggest issue, standardize settlement references.

If outlet evidence is the biggest issue, standardize outlet submission rules.

The win is not zero Evidence Debt.

The win is moving from close-stopping surprises to managed exceptions.

The goal is to be audit-ready by default

Evidence Debt will not disappear overnight.

But it can be managed.

The shift starts when finance stops treating evidence as an attachment problem and starts treating it as a chain problem.

Receipts matter.

Refund records matter.

Payment and settlement records matter.

Consolidated e-Invoice support matters.

But none of those objects are enough if they cannot be connected when pressure arrives.

For multi-outlet F&B finance teams in Malaysia, the standard should be simple:

Transaction evidence should be audit-ready by default across every outlet and payment rail.

That means finance should not need a scavenger hunt to explain what happened.

The proof should already be there.

Run the Proof Gap Diagnostic

If receipt-chasing, refund questions, settlement matching, or e-Invoice support are slowing your close, take the 5-Minute Proof Gap Diagnostic.

It will help you see where your transaction evidence breaks first: retrieval, outlet consistency, payment matching, refund traceability, or close support; and what to fix next.