MVTR: the Minimum Viable Trust Receipt

A receipt is not audit-ready just because it exists. MVTR defines the minimum fields a receipt needs to help finance connect outlet proof, payment proof, settlement proof, refunds, and close support without a manual hunt.

A receipt can exist and still fail finance.

That is the uncomfortable part.

You may have the receipt image. You may have the POS export. You may have the payment approval sitting somewhere in a portal. You may have the settlement report. You may even have the transaction posted correctly in the GL.

But when finance needs to explain one transaction quickly, the evidence does not connect.

The receipt number does not match the payment reference.

The payment reference does not appear on the receipt record.

The settlement arrives as a batch.

The refund does not clearly link back to the original sale.

The outlet says the record exists, but finance still has to search across folders, exports, portals, screenshots, and messages.

That is not a missing receipt problem.

That is a trust problem.

A receipt is useful to finance only if it helps prove what happened.

That is why Proof of Purchase uses the idea of MVTR: the Minimum Viable Trust Receipt.

The problem is not whether the receipt exists

Most teams treat receipts as proof because receipts feel like proof.

They show an amount. A date. A merchant's name. Sometimes an item list. Sometimes a tax or service charge breakdown.

That may be enough for a customer.

It is not always enough for finance.

For a finance team supporting close, audit, refund review, payment reconciliation, or consolidated e-Invoice evidence, the question is not:

Do we have a receipt?

The better question is:

Can this receipt help us retrieve, explain, and defend the transaction?

That is a higher standard.

A receipt that cannot be matched to the POS record, payment approval, settlement batch, refund trail, or GL posting is not audit-ready by default.

It is just an attachment.

And attachments do not reduce proof gaps unless they carry the right links.

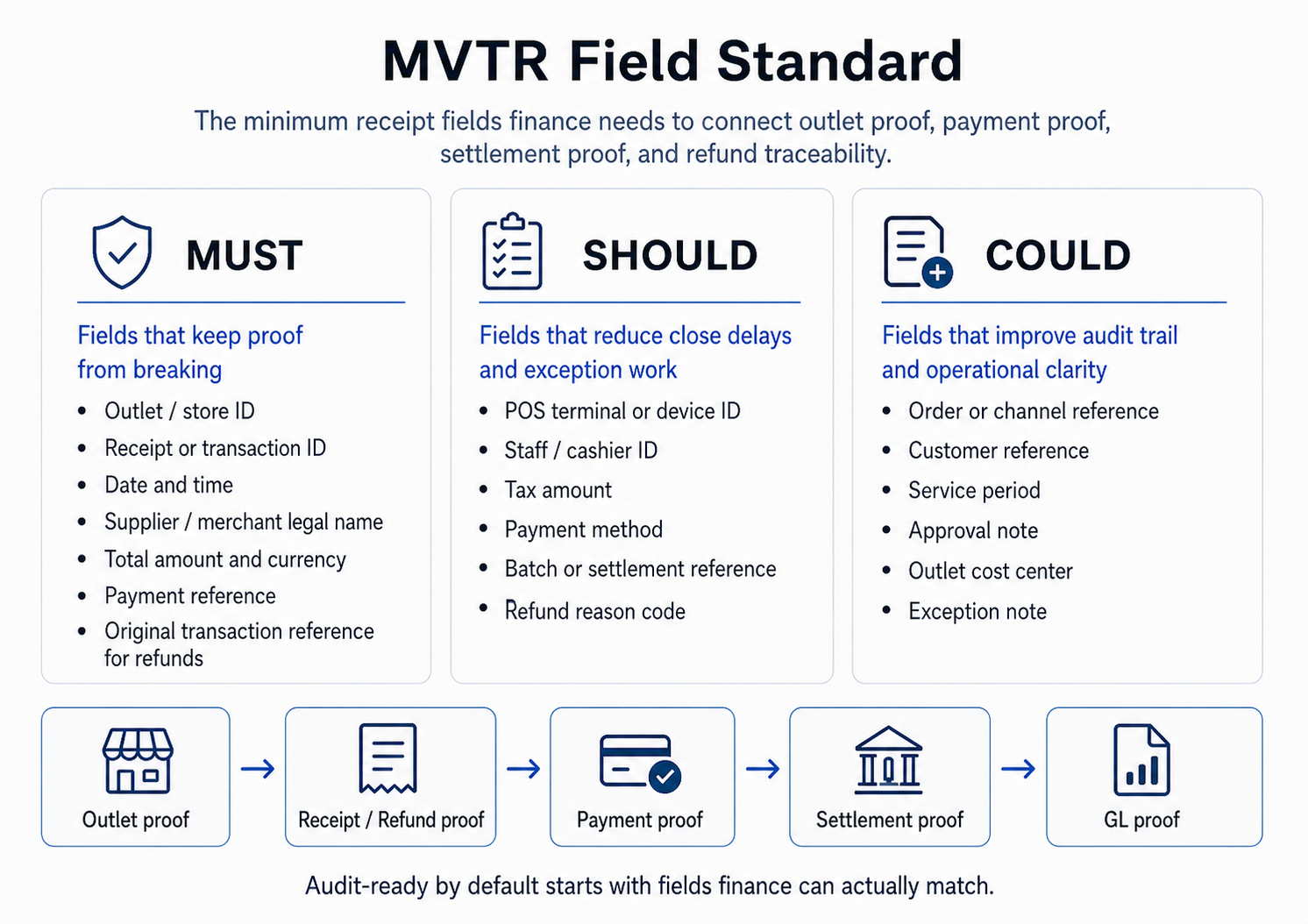

What MVTR means

MVTR stands for Minimum Viable Trust Receipt.

It is the minimum receipt field standard needed to make a receipt useful as transaction evidence.

MVTR does not mean every receipt needs to become complicated.

It does not mean you need to replace your POS system immediately.

It does not mean every outlet needs a new workflow tomorrow.

It means this:

A receipt should carry, or point to, enough information for finance to connect the transaction across the evidence chain.

At minimum, that chain includes:

- outlet proof

- receipt or refund proof

- payment proof

- settlement proof

- GL proof

- consolidated e-Invoice support where relevant

The simplest version is this:

A trustworthy receipt is one that merchant'sfinance can match to payment proof in one search.

If finance cannot do that, the receipt may still be real.

But it is not ready.

Why this matters in multi-outlet F&B

In a single outlet, weak receipt evidence is annoying.

Across many outlets, it becomes operational drag.

A multi-outlet F&B finance team in Malaysia may be dealing with:

- different outlets

- different terminals

- different cashiers

- card payments

- QR payments

- e-wallets

- delivery platform payments

- refunds

- voids

- discounts

- service charges

- daily POS exports

- batched settlements

- consolidated e-Invoice support

Each individual transaction may look small.

But finance does not manage one transaction at a time.

Finance manages the evidence system those transactions create.

If receipt records are inconsistent across outlets, close becomes slower.

If payment references are missing, reconciliation becomes manual.

If refund links are weak, exception review becomes guesswork.

If settlement batches cannot be traced back cleanly, finance has to reconstruct the story.

If supporting evidence is weak, audit and e-Invoice readiness suffer.

This is where Evidence Debt builds.

The work does not disappear.

It moves downstream to finance.

The evidence chain for a receipt needs to support

A receipt sits near the beginning of the transaction evidence chain.

But finance needs the full chain.

A useful receipt should help answer five questions.

1. Where did the transaction happen?

Finance needs clear outlet proof.

That means the receipt should identify the outlet, terminal, timestamp, and transaction status clearly enough to separate one outlet’s activity from another.

If the business has multiple locations, “receipt exists” is not enough.

Finance needs to know which outlet created it.

2. What did the outlet record?

Finance needs the receipt to connect to the POS record.

That includes the receipt number, items or order details where relevant, subtotal, tax, service charge, discount, total amount, currency, and transaction status.

For F&B, this may also include order ID, table ID, staff ID, or cashier ID.

3. How was the transaction paid?

Finance needs payment proof.

A receipt should show or connect to the payment method and the payment transaction reference.

This matters because the payment portal often has its own reference, and that reference may be different from the POS receipt number.

If the payment reference lives only in the payment portal and never appears on the receipt record, finance has to hunt.

4. Where did the money settle?

Finance needs settlement proof.

Settlements are often batched. That is normal.

The problem is not that settlement is batched.

The problem is when finance cannot connect one receipt to one payment approval and then into the correct settlement batch.

That is where small variances become multi-person investigations.

5. What happened if the transaction changed?

Finance needs exception proof.

Refunds, voids, discounts, adjustments, chargebacks, and reversals must connect back to the original transaction.

A refund without a link to the original receipt and payment reference creates avoidable ambiguity.

You may know what happened.

But finance needs proof that travels.

The MVTR field list

MVTR is a practical field standard.

It separates receipt fields into three groups:

- MUST: fields that keep proof from breaking

- SHOULD: fields that reduce close delays and exception work

- COULD: fields that improve audit trail and operational clarity

This is not a legal standard.

It is a finance-readiness standard.

Receipt header: always present

Every receipt record should include:

- receipt ID or receipt number from the POS

- outlet ID or outlet name

- terminal ID or register/device ID

- timestamp, including timezone

- currency

- status: sale, refund, void, or reversal

These fields establish the basic identity of the transaction.

Without them, finance starts with uncertainty.

MUST fields: if these are missing, proof breaks

These are the fields that make the receipt useful across systems:

- total amount paid

- tax and service components where applicable

- payment method

- payment approval result

- payment transaction reference

- merchant identifier if the business uses multiple merchant accounts

The most important field is the payment transaction reference.

That reference should be the one finance can search in the payment portal or processor report.

If you improve only one thing, improve this:

Make the payment transaction reference appear on the receipt record and be searchable.

That one change can reduce a lot of manual proof chasing.

SHOULD fields: these reduce close delays and exception work

These fields are especially useful in multi-outlet F&B environments:

- cashier or staff ID

- order ID or table ID

- discount or promo code

- tip or service charge breakdown

- refund link to the original receipt ID

- refund link to the original payment reference

- reason code for refund or void

Reason codes should be structured wherever possible.

Dropdowns beat free text.

Free text turns exception review into interpretation.

Structured fields make patterns easier to see.

COULD fields: useful, but not always required

These fields may improve traceability, depending on the business:

- customer identifier, only if policy allows

- digital receipt location or document ID

- device ID for businesses with many terminals

- QR code that encodes receipt ID and payment reference

- batch or settlement group tag if the processor provides it

These are not always necessary on day one.

But they can make the evidence chain stronger over time.

The MVTR test (in three questions)

Pick any receipt from last month’s close.

Ask these three questions:

- Which outlet and terminal produced this transaction?

- What payment reference proves approval?

- If this is a refund, void, or reversal, what original transaction does it connect to?

If your team can answer those quickly, the receipt is probably doing its job.

If your team has to search the POS, payment portal, outlet folder, manager’s messages, settlement file, and close workbook before answering, you do not have audit-ready proof by default.

You have a workaround.

And over time, the workaround becomes the workload.

How to start without a big system project

Do not start by boiling the ocean.

Start with one outlet group, one payment method, and one evidence break.

For many teams, card payments are the easiest starting point because the payment transaction reference usually already exists somewhere.

The issue is that the reference may not be carried into the receipt record finance actually uses.

A simple MVTR pilot can look like this:

- Pick one payment method.

- Pick one or two outlets.

- Identify the payment transaction reference finance can search.

- Confirm where that reference appears today.

- Make sure it appears on the receipt record or is stored where finance can retrieve it.

- Test whether finance can match receipt to payment approval in one search.

- Add refunds and voids next by requiring the original receipt ID and original payment reference.

The common pattern is simple:

The reference already exists.

It just does not travel with the proof object finance depends on.

That is the gap MVTR is designed to close.

What MVTR does not solve

MVTR is not the full answer.

It does not replace reconciliation.

It does not remove the need for good outlet discipline.

It does not automatically solve settlement batching.

It does not make every receipt audit-ready by itself.

It does one specific job:

It gives finance a minimum standard for when a receipt can be trusted as part of the transaction evidence chain.

That matters because weak receipt evidence creates downstream work.

Strong receipt evidence supports faster retrieval, cleaner exception review, stronger refund traceability, better close support, and more defensible audit evidence.

The goal is not more receipts.

The goal is better proof.

Start with the Proof Gap Diagnostic

If your finance team still depends on receipts that cannot be matched quickly to payment approvals, refunds, settlement reports, or close support, MVTR is a useful place to start.

But MVTR is only one part of the wider proof system.

The bigger question is where your transaction evidence breaks today.

Is it outlet consistency?

Payment matching?

Refund traceability?

Settlement proof?

Close support?

Consolidated e-Invoice evidence readiness?

Start with the Proof Gap Diagnostic.

It will help you see where your evidence process is most likely to break and what to fix first.